Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways

- Tech comparisons to the dotcom era of the late 1990s are overstated

- Today’s AI leaders are supported by solid fundamentals and real profits

- AI demand continues to outpace supply, leading to significant capex spending

Skywatchers are thrilled this week as a rare geomagnetic storm has created another chance to witness the Aurora Borealis – better known as the Northern Lights. From Alaska to Florida, across nearly two dozen states, people caught glimpses of dazzling waves of green, purple, blue, red, and pink lighting up the night sky. Speaking of things shining bright, the S&P 500 is up ~16% year-to-date, powered by mega-cap gains riding the AI boom. Even with the modest declines this week, the index remains within striking distance of delivering its third straight year of 20%+ returns – a feat achieved only once before (five consecutive years from 1995–1999) in the past 75 years. These sustained tech-driven gains are drawing comparisons to the late 1990s and sparking debate over whether today’s AI enthusiasm is creating a bubble. Below, we break down the concerns and share our perspective:

Artificial intelligence bubble talk ‘lights up’

Tech’s rapid ascent in recent years has invited comparisons to the dot-com era—both fueled by transformative innovations. In the late 1990s, optimism around the internet drove major S&P 500 and NASDAQ gains; today, it’s artificial intelligence. While strong returns don’t necessarily signal a bubble, they do warrant closer attention. Here are a few factors worth monitoring:

- High index concentration: Mega-cap valuations have made the S&P 500 increasingly top-heavy. The technology sector alone accounts for 36% of the index’s market cap, surpassing the dotcom era peak of 34%. Including tech-related names in other sectors – such as Meta, Amazon and the credit card companies – that figure rises above 50%. This concentration means the index’s performance is largely driven by a small group of growth-oriented, tech-related companies, which can narrow market breadth and reduce diversification. While this concentration aligns with our long-term positive view of tech, it’s worth noting that it could lead to risks that need to be managed.

- Lofty valuations: Valuations on the S&P 500 appear stretched. While valuation metrics aren’t precise timing tools, the index is trading in its 99th percentile over the past 20 years – essentially at peak levels. The market is “priced for perfection” and vulnerable to pullbacks from any disappointments. However, higher valuations relative to history are supported by greater exposure to traditionally higher P/E sectors (such as the tech-related companies), stronger profitability metrics, consistent earnings beats and improved visibility into future results.

- Circular financing risks: Recent partnership announcements across the tech ecosystem involve tens of billions of dollars in capital through interconnected relationships. These deals often fund purchases of products or services within the same network, creating a self-reinforcing loop. While collaboration can drive innovation, it’s important to ensure demand is sustainable and supported by underlying cash flows.

Why the AI boom still ‘shines bright’

While some worry that today’s bull market – powered by the AI boom – could echo the dotcom era, we believe those comparisons are overstated. Pullbacks are inevitable and a normal part of any rally, and enthusiasm for new technologies can lead to periods of heavy investment. However, we view this cycle as more structural and long-lasting than speculative.

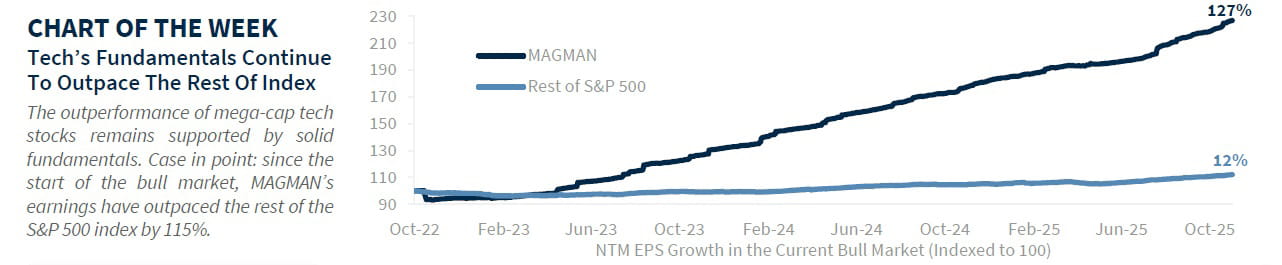

- Strong earnings growth: Unlike the late 1990s, today’s AI surge is driven by companies with solid fundamentals and real profits. Back then, businesses were rewarded simply for having ‘dotcom’ in their name. Today’s AI leaders are profitable and growing. For example, since the start of this bull market, our MAGMAN* composite has increased earnings by 127%, compared to just 12% for the rest of the S&P 500. Better than expected results in 3Q25 reinforce this trend. Even Fed Chair Jerome Powell highlighted the distinction in his recent remarks, noting that AI-related capital spending is now a meaningful contributor to US economic growth. NVIDIA’s earnings next Wednesday will also be key.

- Diversified revenue streams: Another key difference from the dotcom era is the breadth of today’s tech business models. While MAGMAN companies and other big tech firms are investing heavily in data centers, they also generate revenue from diverse sources ranging from hardware to software to streaming services. This diversification provides resilience as AI adoption progresses.

- Greater adoption rates: Technology adoption and the pace of change are far faster today than in the 1990s. Global access to computers and the internet is now widespread, and AI applications reach well beyond consumer-facing tools. Businesses are leveraging AI to manage massive datasets in areas like medical research and mining. Demand for AI continues to outstrip supply – one reason AI-related capital spending by the four largest hyperscalers (Meta, Amazon, Microsoft, Alphabet) is projected to hit $460b in 2026, a 28% increase over 2025 levels. Strong cash flows from these mega-cap companies enable continued investment in the next frontier of technology.

Bottom line

While headlines often speculate about an AI bubble, we believe the long-term outlook for technology remains strong. Periodic volatility is a normal part of any innovation cycle and unlikely to derail our constructive view on equities. We remain positive on the technology sector – along with Industrials, which play a critical role in supporting data center expansion – given durability and transformative potential of the AI megatrend.

* MAGMAN represents a composite of Microsoft, Apple, Google, Meta, Amazon, Nvidia. The foregoing is not a recommendation to buy or sell MAGMAN stocks.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.