Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways

- S&P 500 earnings estimates have continued to move higher

- US energy independence should cushion economic growth

- Despite war, credit spreads have demonstrated notable stability

Recent weeks have been a whirlwind of headlines centered on the Middle East conflict and rising oil and gas prices, particularly as the conflict enters its fourth full week. We’re closely monitoring these developments, not only for their broader military and economic implications, but also to assess whether they warrant any changes to our asset class views. That said, this week we’re taking a step back and widening the lens.

Rather than focusing exclusively on what could go wrong, we’re highlighting 10 things that are going right across the economy and financial markets. These positives can be easy to miss amid a steady drumbeat of war‑related news, but they offer important insight into the underlying resilience shaping the path forward for long‑term investors.

- US military strength: During uncertain times, it is reassuring to know that the US maintains the most powerful military force in the world. Its strength is rooted not only in scale – the US spends roughly $950 billion a year on defense, far exceeding any other nation – but also in technological superiority, highly trained personnel and unmatched global reach. These capabilities underpin our strategic advantage.

- US economy is energy independent: Since the shale oil revolution, the US has become a net energy exporter. At the same time, gains in energy efficiency have made the economy far more resilient to energy shocks, especially relative to import‑dependent regions like Europe and Asia. Along with the Strategic Petroleum Reserve and policy flexibility such as gas tax holidays, these factors help explain why recent oil disruptions have not sparked widespread panic or the long gas lines reminiscent of the 1970s.

- Consumers remain resilient: While gasoline prices are nearing the psychological $4/gallon level, real-time metrics suggest consumer spending has remained resilient up until this point. Year over year, TSA screenings are up 2-3% year over year, restaurant bookings are up 10% and Redbook sales (department store spending) are also up 6.5%. In aggregate, we expect consumer spending growth to remain positive in 2026.

- Productivity gains: The artificial intelligence (AI) boom is a game changer. Rapid and broad-based adoption across the economy has the potential to meaningfully boost productivity, accelerate economic growth and ease inflationary pressures as workers become more efficient. Over time, this shift should translate into stronger profit margins, improve earnings growth and support corporate profitability.

- Tax refunds are up this year: With three weeks remaining until Tax Day, refunds are tracking 12% higher year over year and 14% above the historical average at this point in the season. Total refunds in 2026 could increase by as much as $140 billion, providing a meaningful tailwind to consumer spending and helping to offset rising gasoline prices.

- March’s performance in perspective: March has been a challenging month for asset class performance, with the S&P 500 on track for a 5.7% decline – its worst month since December 2022 – while bonds are down 2.5%. Even so, these near‑term setbacks haven’t derailed the broader trend: over the past year, both asset classes remain firmly positive, with the S&P 500 up 15% and the Bloomberg Agg up 4%.

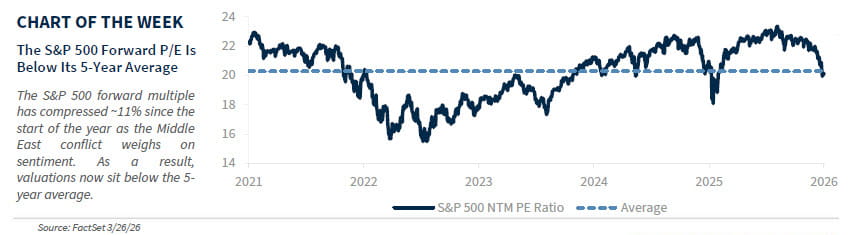

- Equity valuations are normalizing: While valuations were a concern coming into the year, they have normalized meaningfully as earnings revisions have moved higher amid the recent market pullback. Although the S&P 500 has declined ~5% over the past three months, its next 12-month P/E has fallen about 11%, nearly twice what the historical relationship would suggest. As a result, the S&P 500’s NTM P/E now sits below its five‑year average for the first time since last year’s tariff‑related drawdown.

- Earnings estimates moving higher: S&P 500 earnings estimates have surprisingly moved higher since the start of the war. Consensus 2026 earnings are up 2% to $317 per share, implying 17% year-over-year growth, the fastest pace since 2021. Revisions have been broad‑based, with seven of 11 sectors moving higher. Technology continues to lead, with estimates up 6% and earnings growth projected at 40% year over year, the strongest since 2010. With the economy still on solid footing, earnings momentum remains a key tailwind for equities.

- Cash offers an attractive yield: Amid recent market volatility, cash alternatives have emerged as clear beneficiaries. Beyond providing a conservative allocation option, cash now offers an attractive opportunity – with money market yields near 3.7% – allowing investors to earn a reasonable return while patiently waiting to deploy capital as market dislocations create more compelling entry points.

- No significant widening in spreads: Despite heightened geopolitical tensions, credit spreads have remained relatively stable. Since the conflict began, investment‑grade and high‑yield spreads are only two and 17 basis points wider, respectively. This stability suggests markets view the energy shock as a temporary disruption rather than a lasting threat to the corporate outlook.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.